What Investors Look for in AI Companies in 2026: Why Revenue Per Headcount Matters

Updated On:

May 21, 2026

Investors aren't asking "how many people do you have?" anymore. They're asking "how much revenue does each one generate?" That single shift in question is going to separate the companies that scale from the ones that stall.

Here's something that doesn't get said enough: the AI efficiency conversation - and the revenue per headcount metric at its center - is being held in entirely the wrong frame.

Most of the discourse - in boardrooms, in investor decks, in strategy reviews - is circling around headcount reduction. How many roles can AI eliminate? What's the severance exposure? Can we freeze hiring? These are the wrong questions. Because they're operationally shallow. Headcount reduction is a one-time event. Revenue per person is a compounding advantage. And right now, the companies that understand the difference are quietly building something that will be very hard to compete with.

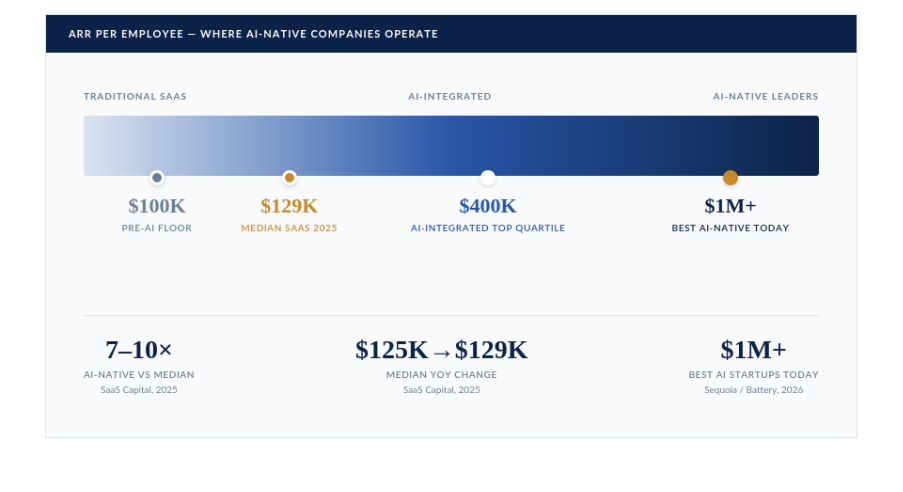

The number that actually matters - the one Sequoia is tracking, the one Battery Ventures is using to separate this generation of AI companies from the last - is revenue per employee. The best AI startups today are generating north of $1 million in revenue per employee.

That's a signal about what the business model of the next decade actually looks like rather than merely being a benchmark.

Why the headcount conversation is a trap

There's a reason the headcount reduction framing is so seductive. It's legible. It shows up cleanly in a cost structure. It makes a CFO feel in control. Cut 20 people, save $3.2 million, done.

But here's what that framing misses entirely: companies that use AI primarily to cut headcount are treating it as an efficiency tax. Companies that use AI to expand what each person can do are treating it as a leverage machine. The latter creates something fundamentally different - a business that grows revenue without growing its cost base proportionally.

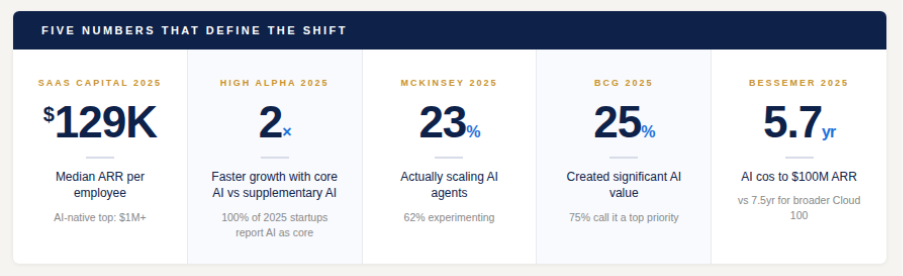

KEY INSIGHT - SaaS Capital, 2025 $129,724

Median ARR per employee for private SaaS companies in 2025, up from $125,000 the prior year. The median is climbing slowly. The interesting story is what's happening at the top end, where AI-native companies are operating at 7–10× this figure.

That's the efficiency story worth telling. And it's still largely untold. The real structural shift isn't in what companies are eliminating. It's in how much a single person can now hold - how many customers they can serve, how many decisions they can make with good data, and how wide a product surface they can own without burning out or bottlenecking growth.

Why Is Headcount Reduction the Wrong Way to Think About AI Efficiency and Why Revenue Per Employee Is?

Headcount reduction is a one-time event with a fixed ceiling. Cut twenty people, save $3.2 million, done and the next growth phase requires hiring them back. The companies using AI to expand what each person can accomplish are building something structurally different: a business where revenue grows without the cost base growing proportionally. AI-native companies scaling faster than SaaS companies are doing so because each person can now hold a product surface, a customer book, or an operational scope that previously required three or four. That is a compounding advantage, not a one-time efficiency gain and investors in 2026 are increasingly pricing the difference.

The compound startup - what investors are actually funding now

The compound startup model is an AI GTM strategy that lets lean teams cover market surface that used to require ten times the headcount.

Sophisticated investors in 2026 are backing a clear pattern: AI-native businesses solving multiple connected customer problems while keeping the human-to-revenue ratio low and expanding product surface.

Earlier SaaS businesses needed separate teams for support, onboarding, account management, sales ops, and analytics - every function required headcount, and headcount constrained margins.

AI-native businesses have pushed that ceiling higher. AI now handles query resolution, onboarding, churn detection, buyer-seller matching, and issue triage - letting a 30-person team do what once required 200. Revenue follows product surface, not org chart size.

KEY INSIGHT - High Alpha, 2025 SaaS Benchmarks 2× faster growth

SaaS companies with AI deeply integrated into their core product grow twice as fast as those using AI as a supplementary feature. 100% of companies founded in 2025 report AI as core to their product. The baseline has shifted - the question is no longer whether you have AI, but whether it's doing compound work or decorative work.

That's a structural divergence, not a marginal improvement. Two companies in the same category, selling to the same buyers, with the same market opportunity - one growing at twice the rate of the other, not because of better salespeople or a bigger brand, but because of how deeply AI is embedded in the product architecture.

What compound work actually looks like at the operational level

This is where the conversation usually gets vague, so let's make it concrete.

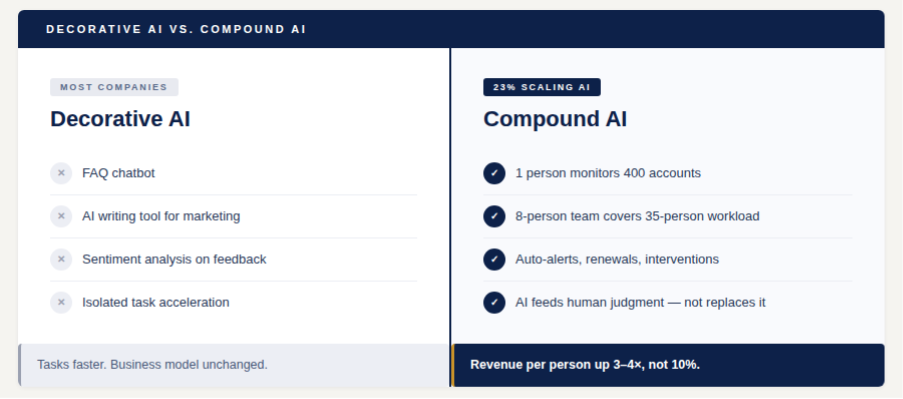

Decorative AI work: a chatbot for FAQs, an AI writing tool for marketing, sentiment analysis on customer feedback. Each useful. None of them change the structural economics of the business. They make individual tasks faster. They don't change how many customers one person can serve.

Compound AI work: a customer success function where one person monitors 400 accounts simultaneously - proactive alerts on usage drops, recommended intervention scripts, auto-drafted renewal emails, real-time product health data, no dashboard-switching required.

The outcome isn't firing the CS team, it's your 8-person team covering a book of business that previously required 35, at higher quality, with better data.

"AI is not about job loss. It's about workforce transformation."

- Gartner

That's the compound effect. It's not about subtraction. It's about what the same headcount can now hold. And the organizations that architect for this - rather than bolting AI onto existing workflows - are the ones building a cost structure that gets better as they scale, not one that simply resets after a round of cuts.

KEY INSIGHT - McKinsey, State of AI Global Survey 2025 62% experimenting. 23% scaling.

62% of organizations are already experimenting with AI agents, with 23% scaling at least one agentic system. The gap between experimenting and scaling is where the compound advantage gets built. The 23% in production with agents aren't just ahead on a technology curve - they're running a fundamentally different cost structure.

The gap between aspiration and execution - and why it's an opportunity

Here's the uncomfortable part of this story. Despite the overwhelming directional pressure toward AI-native efficiency, most companies aren't there yet. And that gap is exactly where competitive advantages get built.

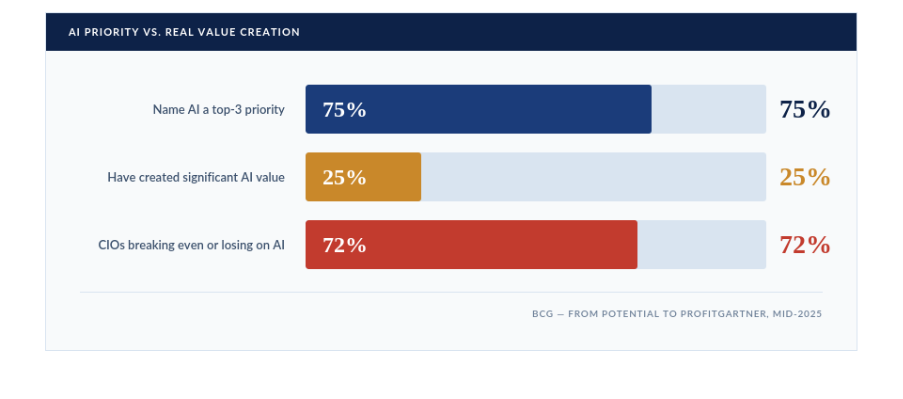

KEY INSIGHT - BCG, From Potential to Profit 75% prioritise it. 25% benefit from it.

75% of executives name AI as a top-three strategic priority for 2025, yet only one in four say their companies have actually created significant value from it. Leading companies allocate more than 80% of AI investments to reshaping functions - not just automating tasks within them.

Gartner's research adds a dimension that doesn't get discussed enough: 72% of CIOs reported in mid-2025 that their organizations are either breaking even or losing money on AI investments. That's the majority of large organizations spending on AI without seeing the returns yet. The companies that solve this first will be operating in a category of one while everyone else is still trying to justify the spend to their boards.

"Winning with AI is a sociological challenge as much as a technological one. The soft stuff turns out to be the hard stuff."

- BCG

The valuation signal that confirms this is the right frame

If you need a market signal to validate the revenue-per-person thesis, look at what's happening at the top of the private cloud market.

KEY INSIGHT - Bessemer Venture Partners, Cloud 100 Benchmarks 2025 $1.1 trillion aggregate value

Cloud 100 honorees now collectively exceed $1.1 trillion - a 36% increase from 2024. AI leaders command 42% of the total list value, doubling from 21% just one year prior. AI companies are reaching $100M ARR ("Centaur" status) in 5.7 years on average - a full year faster than the previous cohort.

In one year, the market's allocation to AI-native companies inside the top tier of private cloud businesses went from one-fifth to nearly half. That's a recalibration of what the market believes a scalable business actually looks like, not a trend.

Speed to scale is accelerating because the structural constraints that used to slow companies down - needing to hire before you could serve more customers - no longer apply in the same way. You can expand product surface and customer capacity without the corresponding headcount ramp.

The economics look nothing alike.

"Building with AI is no longer a differentiator - it's the baseline." - High Alpha, 2025 SaaS Benchmarks

Battery Ventures called this moment accurately: the SaaS 1.0 playbook is officially obsolete. Companies that grew by hiring sales reps to penetrate new segments, support agents to retain existing customers, and ops teams to manage complexity - that model is being replaced.

The new model grows by making AI more capable, not by adding more people.

What Metrics Are Investors Using to Evaluate AI Startups in 2026? (Hint: It's Revenue Per Employee)

ARR and growth rate still matter, but in 2026 the real separator is revenue per employee.

The best AI-native startups exceed $1M per employee, signaling AI is driving compounding work, not decorative features. Investors also look for net revenue retention above 120%, AI as a core product component, and a cost structure that improves as revenue scales.

The "compound startup" - lean teams, wide product surface, AI-native operations - is what VC funding is increasingly built around.

What This Means for How You Build, Fund, and Evaluate Your AI GTM Strategy

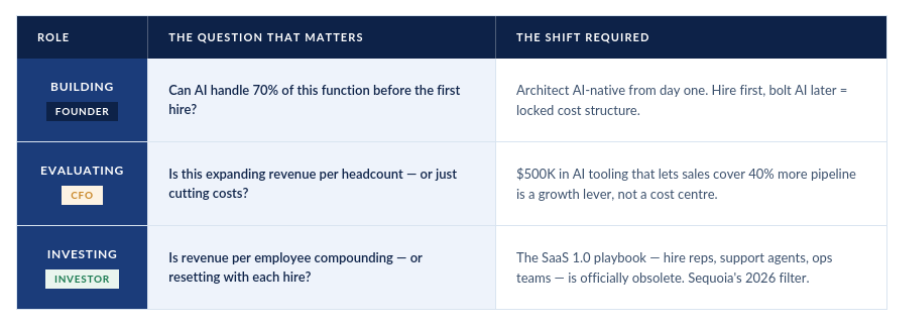

If you're building: before every new hire, ask whether AI can handle 70% of the work first. Not to avoid hiring but because hiring first and bolting AI on later locks in a cost structure that's harder to change than you think. Companies architecting AI-native workflows from the start are the ones hitting revenue-per-employee numbers that attract the next round at a valuation worth celebrating.

If you're evaluating: stop benchmarking AI ROI against cost savings. Benchmark it against revenue expansion per unit of headcount. A $500K investment in AI tooling that lets your sales team cover 40% more pipeline with the same headcount isn't just a cost centre, it's also a growth lever. The framing determines what you measure, and what you measure determines what you build toward.

If you're investing: Sequoia's framing for 2026 is that the conversation is moving from the "$0 to $100M club" to the "$0 to $1B club."

The companies that will get there aren't the ones with the biggest teams or the most funding. They're the ones that have figured out how to make revenue per person a compounding advantage rather than a fixed ratio.

Conclusion: Three verdicts, one principle

1 - The headcount story is the wrong story. Cutting people is a one-time gain with a fixed ceiling. Building a business where each person generates more revenue over time because AI handles what used to require three additional hires - is a compounding structural advantage. Companies fixated on the former will hit their ceiling. The ones building for the latter won't see one for a while.

2 - Revenue per employee is the metric that matters. It captures whether AI is doing decorative or compound work inside your business. It's what separates the 25% generating real value from the 75% still justifying the investment. And it's what investors are increasingly using to underwrite the next round, the next valuation, and the next category winner.

3 - The architecture and the AI GTM strategy has to come first. The companies defining the next generation of enterprise software aren't the ones that added AI tools to existing workflows. They're the ones that restructured how work flows around AI from the start and built the operational architecture to make revenue per person a ratio that compounds as they scale.

The organizations still asking "how do we use AI to cut costs" are playing a different game than the ones asking "how do we use AI to change how much one person can generate." One of those questions has a ceiling. The other one doesn't. That's the distinction that will still matter five years from now, long after the current hype cycle has flattened and the real structural advantages have already been locked in.