How Outcome-as-a-Service and Outcome Based Pricing Are Changing SaaS GTM

Updated On:

May 21, 2026

The subscription model isn't dying. But it is, quietly and unevenly, beginning to lose on a new dimension.

The companies that recognize outcomes as a competitive variable before their competitors do won't just win more deals but also define what the entire category charges for and that's a far more durable advantage than any feature on a roadmap.

The Subscription Is Not Dying. But It's Losing.

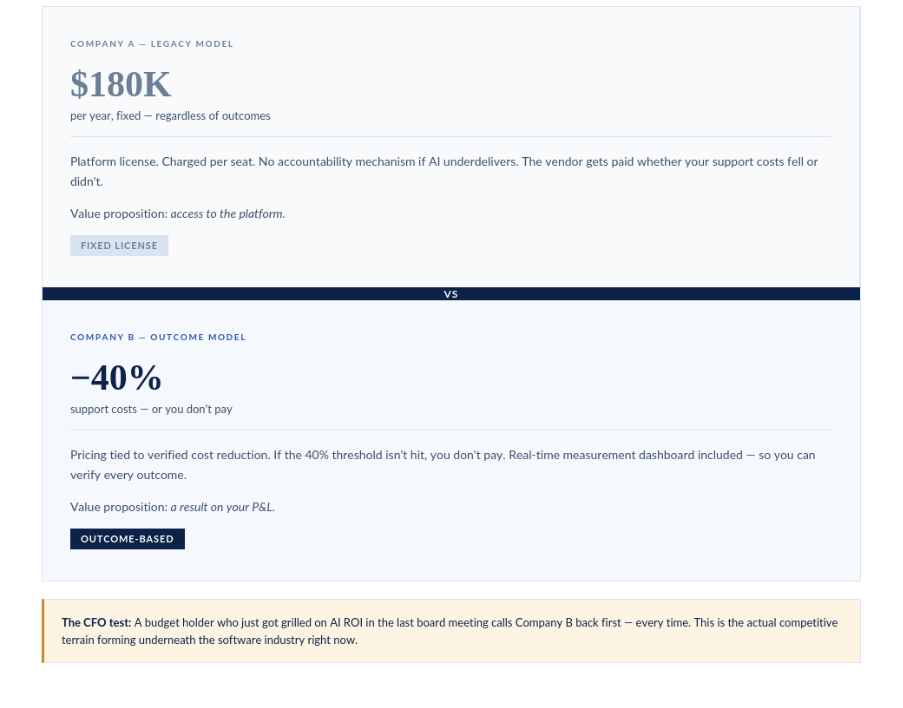

Here's a scenario worth sitting with. Two companies sell AI-powered customer support automation. Company A charges you a platform license - $180,000 a year, fixed, regardless of outcomes. Company B says: "We'll reduce your support costs by 40%. If we don't hit that number, you don't pay."

Now ask yourself - not as a technologist, but as a CFO who just got grilled about AI ROI in the last board meeting - which vendor do you call back?

This isn't hypothetical but actual competitive terrain forming underneath the software industry right now, and most companies haven't fully reckoned with what it means for how they price, how they sell, and ultimately, how they survive.

The Shift Nobody Is Talking About Loudly Enough

Most of the AI conversation in 2025 is about capability. Which model is better. Whether agents can replace knowledge workers. How fast things are moving. These are interesting debates - but they're not the debate that will determine which software companies are still standing five years from now.

The debate that matters is a pricing debate. More specifically, it's a debate about whether outcome based pricing becomes the default commercial model for AI-native software categories.

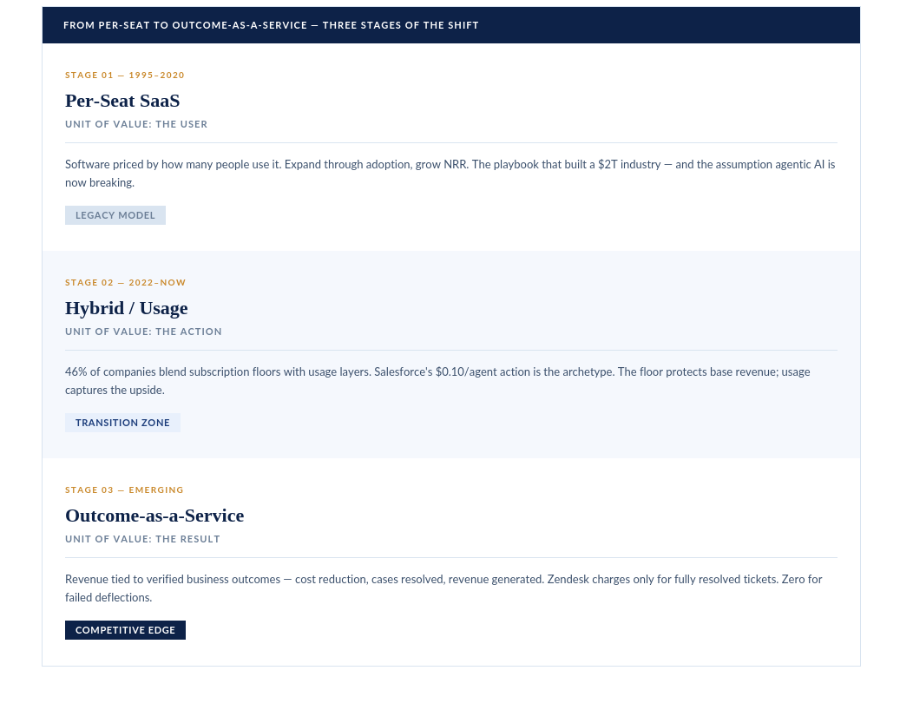

For three decades, SaaS built an extraordinary industry on a simple idea: charge per seat, expand through adoption, grow net revenue retention. It worked because software was a tool, and tools were priced by how many people used them. The unit of value was the user.

Agentic AI quietly broke that logic. When a single AI agent can do the work of five support reps, ten data analysts, or an entire onboarding team, the per-seat model stops being a pricing strategy and starts looking like a legacy assumption. As the a16z framing of this shift puts it plainly: software is becoming labor. And labor has never been priced by the seat. Labor is priced by output.

This is what "Outcome as a Service" actually means - not a rebrand, not a marketing pivot, but a fundamental repricing of where value is captured in the software stack. And to be precise: this isn't about SaaS dying.

The subscription model isn't going anywhere. What's changing is that outcomes are becoming a competitive variable - a new dimension on which vendors will increasingly win or lose - layered on top of the existing commercial landscape.

Why Is SaaS Pricing Being Disrupted by Outcome as a Service Models in AI Companies?

The per-seat pricing model was built for a world where software was a tool used by people. Agentic AI broke the unit of value: when a single agent can do the work of ten support reps, per-seat pricing stops being a commercial strategy and starts looking like a legacy assumption. Companies moving to performance-based pricing in AI are not making a marketing decision — they are responding to buyers who have stopped tolerating the gap between what the vendor promises and what the contract guarantees. Outcome-based pricing collapses that gap by design. It forces the vendor to price on what the customer actually cares about: results, not access.

What Zendesk and Salesforce Are Actually Signaling

The companies worth watching aren't announcing this shift loudly. They're quietly pricing around it.

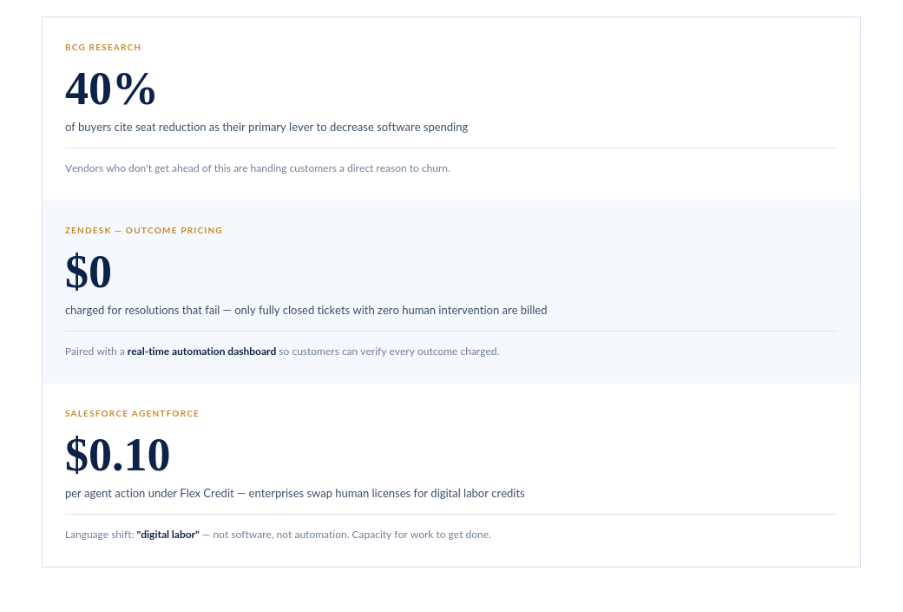

Zendesk was first among major CX platforms to introduce outcome-based pricing tied to automated resolutions - cases fully closed by AI, zero human intervention. Not deflection. Resolution. They paired it with a real-time automation dashboard, because if you're charging for outcomes, customers need to verify them. That dashboard is what makes the pricing model credible.

Salesforce followed a parallel path with Agentforce's Flex Credit - $0.10 per agent action - structured so enterprises can actively swap human licenses for digital labor credits. The language matters: digital labor, not software, not automation. They're signaling that what they sell is no longer platform access. It's capacity for work to get done.

KEY INSIGHT: 40% of buyers already cite seat reduction as their primary lever to decrease software spending, according to BCG. Vendors who don't get ahead of this are handing their customers a reason to churn.

Both of these are early-stage experiments. The attribution challenges are real, the measurement infrastructure is still being figured out, and the pricing mechanics will evolve. But the direction is unmistakable.

Why This Matters More Than Technical Superiority

This is the part that should make any founder or product leader genuinely uncomfortable.

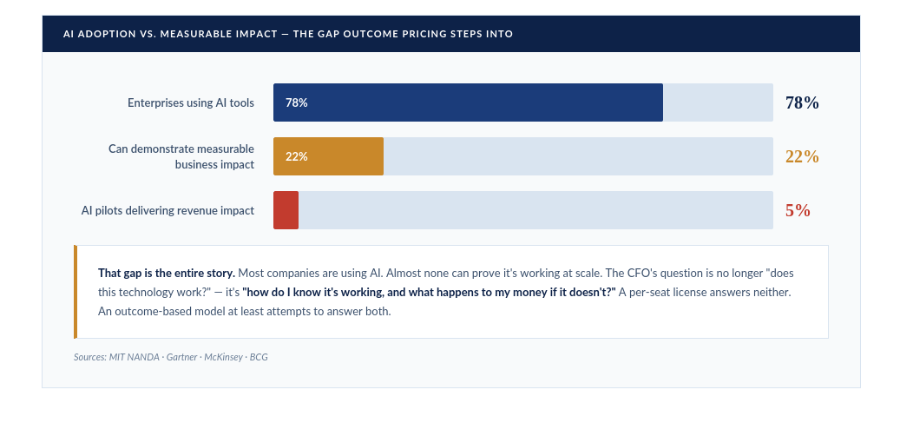

You could build the best agentic AI system in the market - better recall rates, lower latency, more reliable reasoning than anything a competitor ships - and still lose. Not because your product is worse, but because your pricing model makes it structurally harder for a risk-averse CFO to say yes.

The data tells you exactly why this dynamic is so powerful right now:

That's why outcome pricing is increasingly functioning as a trust signal. The willingness to tie your revenue to a result communicates something about your confidence in your own product that a fixed annual license simply cannot.

The Real Bottleneck: Attribution

Here's where the honest conversation gets harder.

Outcome-based pricing sounds compelling until you hit enterprise software's hardest problem: attribution. How do you prove a result was caused by your product, and not a process change, a seasonal trend, or the five other tools running simultaneously?

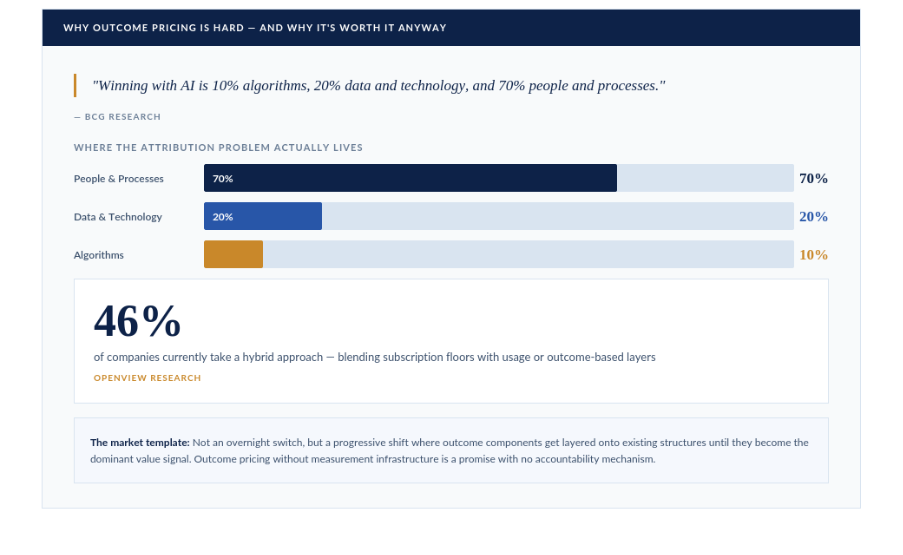

The attribution problem is organizational, not technical - requiring baseline measurement before deployment, contractual clarity around what counts as an outcome, and instrumentation most vendors have never had to build.

Zendesk's automation dashboard exists for exactly this reason. Outcome pricing without measurement infrastructure isn't a pricing model but a promise with no accountability mechanism. CFOs controlling AI budgets know the difference.

That's why the transition will be gradual. Outcome components will layer onto existing pricing structures until they become the dominant value signal, not replace them overnight.

What Pricing Model Should AI Startups Use: SaaS Subscription, Outcome as a Service, or Outcome-Based Pricing?

The answer depends on how defensible the attribution is. Subscription pricing is lower risk and operationally simpler - it works well when the product is a platform or tool that augments human work rather than replacing a measurable business outcome.

Outcome-based pricing is higher reward and higher commitment: it wins more deals with financially conservative buyers, builds trust through skin-in-the-game positioning, and can command premium pricing when the outcome is clearly defined. The practical template for most AI startups is a hybrid - a base subscription that reduces commercial risk, layered with an outcome component that grows as the attribution infrastructure matures.

The companies that figure this out first will not just win more deals but also set what the category charges for.

The AI GTM Strategy Implications Nobody Wants to Sit With

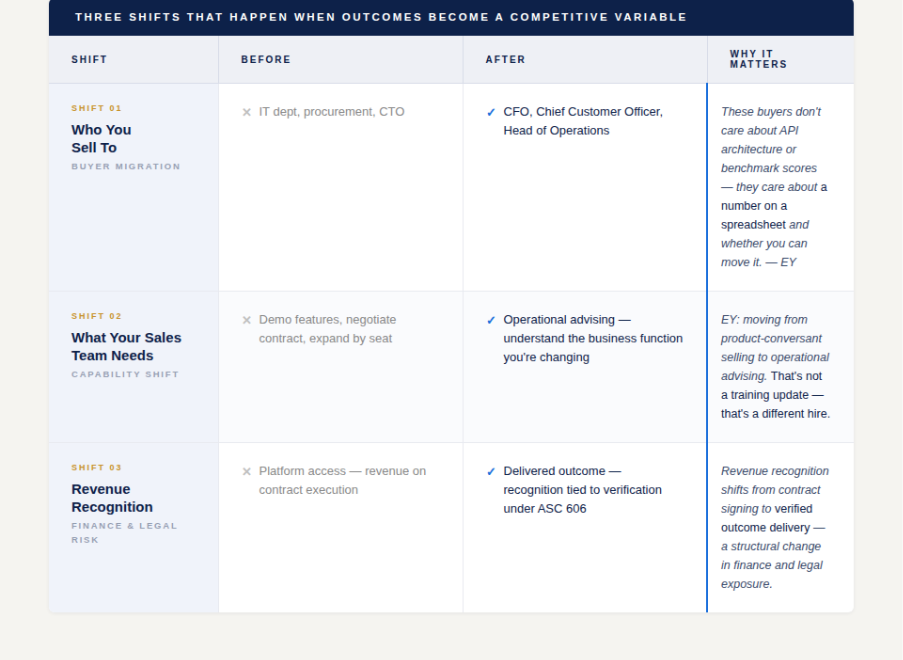

If outcomes become a competitive variable, the go-to-market motion has to change - and not in comfortable ways. That shift is fundamentally redefining what an AI GTM strategy looks like in enterprise software.

Here's how the model actually shifts across three dimensions:

The first shift is who you sell to. EY's research on agentic AI go-to-market strategy is clear: buying decisions are moving away from IT departments toward business leaders like the CFO, Chief Customer Officer, and Head of Operations. These buyers don't care about API architecture or benchmark scores. They care about whether you can move a number on a spreadsheet.

The second shift is what sales teams need to know. The traditional enterprise software playbook - demo features, negotiate contracts, expand by seat - starts breaking down when the value being sold is a business result rather than platform access. EY describes this as moving from product-conversant selling to operational advising. That's not a training update. It's a different hire.

The third shift - and the one finance teams consistently miss - is revenue recognition. Under ASC 606, selling platform access and selling delivered outcomes are legally different models. Outcome-based contracts change how and when revenue hits the income statement, affecting forecasting and quarterly visibility. Finance and legal need to be involved from day one.

KEY INSIGHT: The buying criteria shift is already underway. EY's research confirms that enterprise software decisions are actively migrating from IT departments to business function leaders. If your sales motion still leads with a product demo, you are already behind.

The Companies That Figure This Out First Will Set the Category Standard

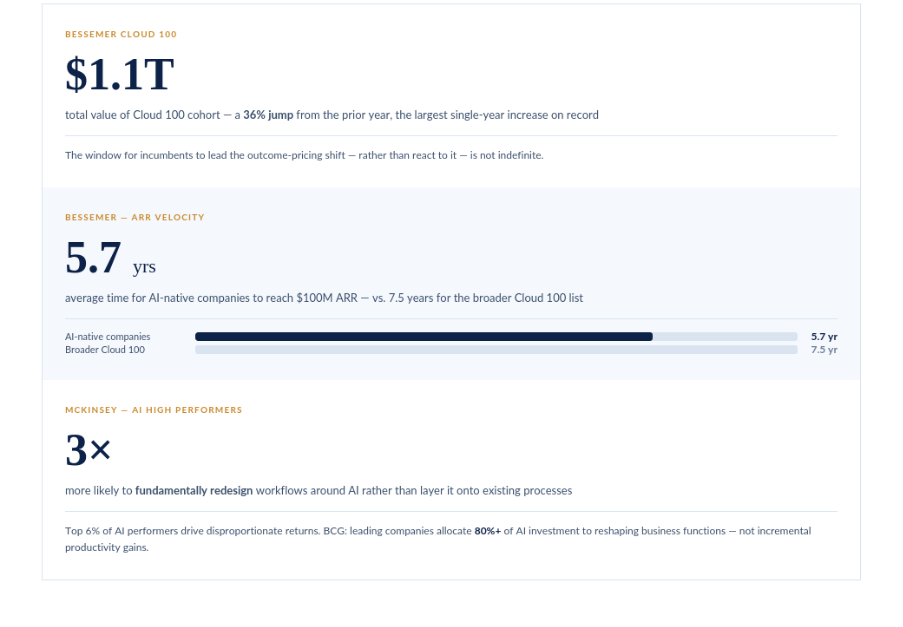

McKinsey's research on AI high performers - the top 6% generating disproportionate returns - found one consistent pattern: they were three times more likely to redesign workflows around AI instead of layering it onto existing processes. BCG found something similar: leading companies allocate more than 80% of their AI investment toward reshaping business functions rather than incremental productivity gains.

The same logic applies to vendors. The companies that win in an outcome-competitive market won't necessarily have the best models. They'll be the ones willing to restructure pricing, customer success, sales hiring, and measurement infrastructure around a different definition of value delivered.

The urgency is real. Bessemer's Cloud 100 data shows the cohort crossed $1.1 trillion in total value for the first time - up 36% year over year. AI-native companies are reaching $100M ARR in 5.7 years on average versus 7.5 years for the broader market, with some hitting it in under four years. The window for incumbents to lead this shift instead of reacting to it is not indefinite.

The companies that move first aren't just winning deals; they're defining what a winning AI GTM strategy looks like for the entire category.

KEY INSIGHT: The companies reaching scale fastest aren't winning on product alone. They're winning on how they frame, price, and prove value and that playbook is being rewritten right now.